|

| Not the place of the dinner, but illustrative |

Last night I gave a ride to a guy who interviews “founders” of successful tech companies for his podcast. Basically they are serial entrepreneurs responsible for creating many tech companies. The best of the best.

There was a big dinner for these founders, who are in Austin for the South By Southwest event (SxSW).

21 founders were invited 17 showed up.

The dinner was in a mansion in the Tarrytown neighborhood of Austin, it was catered by a five star chef. The entire cost was underwritten by a finance firm called Mercury (https://mercury.com/ ) seeking their business.

Tarrytown is a big oak tree lined neighborhood of gorgeous southern mansions, close to downtown Austin. This is where old money lives. Or at least used to. I suspect many of the properties may be high end AirBNBs for the well off. It’s only a mile or two from downtown.

My rider was on the phone talking to someone about how many of these founders are having 10 and 20 million dollar credit lines yanked despite having high cash on hand ratios in their companies and cash flows that exceed their credit lines. They weren’t given a reason for the credit lines being yanked. And they were taking their entire banking business and cash to other places. Whatever was going on, the bank revoking the credit lines made them all very nervous.

Some went to Mercury, and others were looking for new banks that could offer the liquidity they needed. A lot of them are getting twitchy and cutting overhead as quickly as they can. And they were spreading the word about whatever bank it was in Silicon Valley that is yanking credit lines. Many were affected. The specific bank in contraction was not named.

As a driver I’m one of the invisible people, like barbers, hair stylists, waitresses and bartenders. Sometimes people tell you the most amazing things they wouldn’t tell anyone else. They’re pretty sure they’ll never see you again and that is often true and they need to tell somebody. Other times you overhear the cell phone calls like last night. Odd I’d be the driver but that’s pretty much how the last 10 years have been for me. No coincidences.

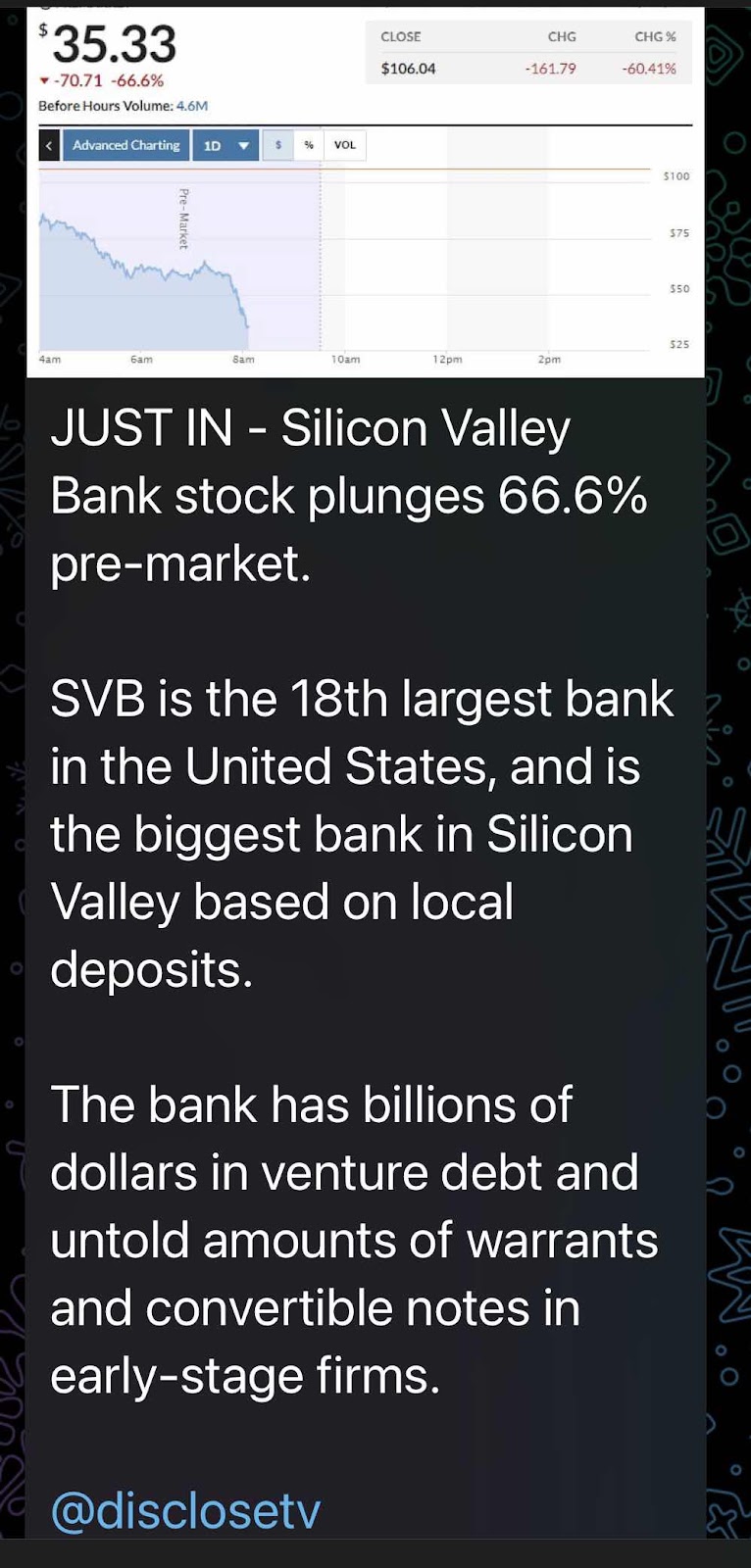

The first thing this morning I noticed this new on the @disclosetv Telegram feed.

Banks gamble, that's how they lose money. They don't risk their own capital when they make you a loan, they convert your promissory note to IRS OID (sp?) form (the IRS is the middle man in the funds transaction), which is then forwarded to the Federal Reserve, which remits the funds for your loan via Fedwire from your value held at the Fed. So with that kind of free money loaned out at market rates, how could a bank ever go broke? Only if they gamble their free money.

SVB gambled on Silicon Valley startups, some of which succeed and produce a new service or product. Other large banks gamble in derivatives and exotic financial products that take a mathematician with knowledge of differential equations to even be able to guess their risk and reward potentials. It also funded a lot of hare brained "green companies" and solar panel companies.

It doesn't take a genius to guess which bank was actually risking money on real ventures that could bring wealth to many people. So something in all this feels off... then there's the personnel links to key people from failed banks in 2008... and it kind of underscores the setup here. And they made sure they paid themselves first!

There was a big dinner for these founders, who are in Austin for the South By Southwest event (SxSW).

21 founders were invited 17 showed up.

The dinner was in a mansion in the Tarrytown neighborhood of Austin, it was catered by a five star chef. The entire cost was underwritten by a finance firm called Mercury (https://mercury.com/ ) seeking their business.

Tarrytown is a big oak tree lined neighborhood of gorgeous southern mansions, close to downtown Austin. This is where old money lives. Or at least used to. I suspect many of the properties may be high end AirBNBs for the well off. It’s only a mile or two from downtown.

My rider was on the phone talking to someone about how many of these founders are having 10 and 20 million dollar credit lines yanked despite having high cash on hand ratios in their companies and cash flows that exceed their credit lines. They weren’t given a reason for the credit lines being yanked. And they were taking their entire banking business and cash to other places. Whatever was going on, the bank revoking the credit lines made them all very nervous.

Some went to Mercury, and others were looking for new banks that could offer the liquidity they needed. A lot of them are getting twitchy and cutting overhead as quickly as they can. And they were spreading the word about whatever bank it was in Silicon Valley that is yanking credit lines. Many were affected. The specific bank in contraction was not named.

As a driver I’m one of the invisible people, like barbers, hair stylists, waitresses and bartenders. Sometimes people tell you the most amazing things they wouldn’t tell anyone else. They’re pretty sure they’ll never see you again and that is often true and they need to tell somebody. Other times you overhear the cell phone calls like last night. Odd I’d be the driver but that’s pretty much how the last 10 years have been for me. No coincidences.

The first thing this morning I noticed this new on the @disclosetv Telegram feed.

Silicon Valley Bank is owned by Silicon Valley Group. It’s top 10 shareholders include Vanguard and Blackrock. Share trading was halted after its shares dropped 66.6%. Interesting digits.

SVB was co-conceived by a guy named Bill Biggerstaff. I know, I laughed too!

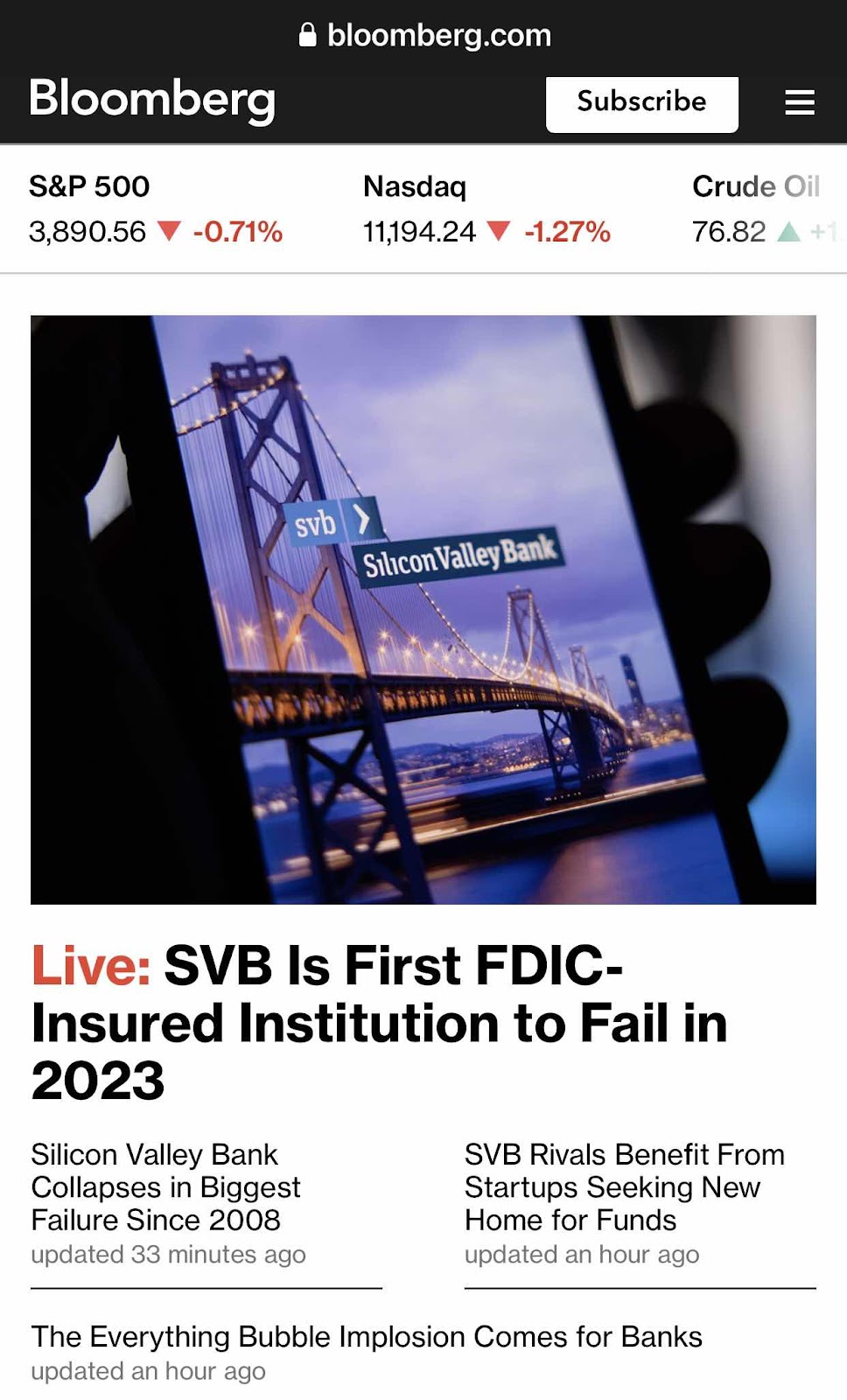

Then it hit Bloomberg.

Update 1:

Update 2:

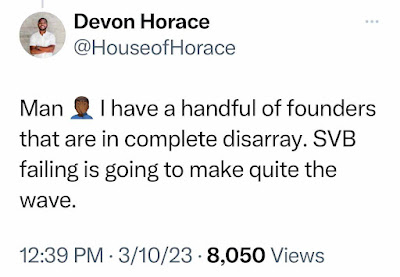

https://twitter.com/houseofhorace/status/1634262735763705858?s=46&t=l3cvDrPl83_cjLIo4dxr5w

Update 3:

Banks gamble, that's how they lose money. They don't risk their own capital when they make you a loan, they convert your promissory note to IRS OID (sp?) form (the IRS is the middle man in the funds transaction), which is then forwarded to the Federal Reserve, which remits the funds for your loan via Fedwire from your value held at the Fed. So with that kind of free money loaned out at market rates, how could a bank ever go broke? Only if they gamble their free money.

SVB gambled on Silicon Valley startups, some of which succeed and produce a new service or product. Other large banks gamble in derivatives and exotic financial products that take a mathematician with knowledge of differential equations to even be able to guess their risk and reward potentials. It also funded a lot of hare brained "green companies" and solar panel companies.

It doesn't take a genius to guess which bank was actually risking money on real ventures that could bring wealth to many people. So something in all this feels off... then there's the personnel links to key people from failed banks in 2008... and it kind of underscores the setup here. And they made sure they paid themselves first!

Kill Silicon Valley startups and only the largest players remain. This is financial herbicide on the most inventive part of the American economy.